Economic Momentum Fades as Q4 GDP Revised Lower

The U.S. economy ended 2023 on a softer note than initially reported, with fourth-quarter Gross Domestic Product growth revised down to a modest 0.7% annualized rate. This downward revision signals a notable deceleration from the robust growth seen earlier in the year, raising questions about the economy’s resilience in the face of elevated interest rates. The slowdown reflects weaker consumer spending and business investment than previously estimated.

This cooling aligns with the Federal Reserve’s goal of moderating economic activity to curb inflation. However, the magnitude of the slowdown introduces new concerns about the potential for an overly restrictive policy stance. Market participants are now closely monitoring whether this represents a temporary soft patch or the beginning of a more pronounced downturn.

Inflation Proves Persistent, Complicating the Fed’s Path

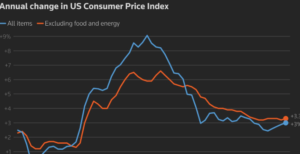

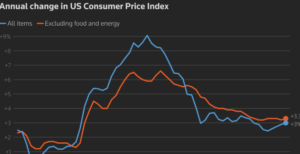

Adding complexity to the economic picture, the latest inflation data remains stubborn. The core Personal Consumption Expenditures (PCE) price index, the Fed’s preferred inflation gauge, registered a 3.1% year-over-year increase in January. This figure matched market expectations but remains well above the central bank’s 2% target.

The headline PCE index, which includes volatile food and energy prices, came in at 2.9% for the same period. While this shows progress from the peaks of 2022, the persistent nature of core inflation, which strips out those volatile components, suggests underlying price pressures are still entrenched in the services sector and wage-driven dynamics.

Market Reaction and Interest Rate Expectations

Financial markets digested this mixed data with caution. Treasury yields showed limited movement, reflecting a market that has largely priced in a patient Fed. Equity markets initially wobbled on the growth revision but found some support in the notion that the Fed might be less inclined to hike rates further with growth slowing.

Futures markets continue to price in a high probability that the Federal Reserve will hold its benchmark interest rate steady at its next meeting. The focus has shifted from the timing of the next rate hike to the timing of the first rate cut, with expectations for initial easing being pushed later into 2024 based on the sticky inflation readings.

The Fed’s Delicate Balancing Act

The juxtaposition of slowing growth and persistent inflation presents a classic policy dilemma for the Federal Reserve. Officials must weigh the risk of overtightening and causing unnecessary economic damage against the risk of declaring victory on inflation too early and allowing price pressures to reaccelerate.

Recent commentary from Fed officials has emphasized a data-dependent approach, with many stating they need to see more consistent evidence that inflation is moving sustainably toward 2% before considering rate cuts. The January core PCE reading does not provide that confidence, likely reinforcing a “higher for longer” stance.

Broader Economic Context and Outlook

The current economic landscape is characterized by a resilient labor market, which continues to support consumer spending, but at a moderating pace. Job growth has slowed from its torrid 2023 pace but remains positive. Consumer confidence readings have been mixed, reflecting concerns over prices and borrowing costs.

Business sentiment surveys, such as those from the Institute for Supply Management (ISM), have shown manufacturing in contraction while services continue to expand, albeit at a slower rate. This bifurcation adds another layer of complexity to the growth narrative and the Fed’s policy calculus.

Implications for Investors and Portfolios

For investors, this environment suggests continued volatility and a premium on selectivity. Sectors sensitive to interest rates, like technology and real estate, may face headwinds if rates remain elevated. Defensive sectors and companies with strong pricing power and resilient earnings could outperform in a slowing growth, sticky inflation scenario.

The U.S. dollar’s trajectory is also key. A strong dollar, often supported by higher relative U.S. interest rates, can pressure multinational corporate earnings and emerging market assets. Conversely, any signal that the Fed is nearing a pivot could weaken the dollar and provide a tailwind for international and commodity-sensitive investments.

Summary and Forward Look

The U.S. economy is navigating a narrow path, with growth cooling to 0.7% in Q4 while core inflation holds firm at 3.1%. This combination challenges the Federal Reserve’s next move, forcing a careful balance between fighting inflation and avoiding a downturn. Market expectations for rate cuts have moderated in response to the persistent price data.

Looking ahead, the focus will shift to upcoming labor market reports and subsequent inflation readings. The Fed’s preferred outcome remains a “soft landing,” where inflation returns to target without a severe recession. However, the latest data underscores the difficulty of that task, suggesting a prolonged period of economic uncertainty and cautious monetary policy.

Comments are closed.