Hormuz Chokepoint Disruption Sparks Fertilizer Supply Fears

The strategic Strait of Hormuz, a vital maritime corridor for global energy and commodity shipments, faces renewed disruption risks due to escalating regional tensions involving Iran. Recent incidents and heightened military posturing have raised immediate concerns over the secure passage of vessels, including those carrying critical agricultural inputs. This uncertainty directly threatens the flow of potash, urea, and phosphate fertilizers from key Middle Eastern producers to global markets.

Approximately 20-30% of the world’s seaborne traded potash, a key potassium-based fertilizer, transits through the Strait. Major producers and exporters in the region, including Jordan and Iran itself, rely on this route. Any significant or prolonged shipping delay or insurance cost increase creates a tangible supply chain bottleneck. Market participants are now assessing the potential for a repeat of the logistics snarls witnessed during past regional flare-ups.

Agricultural Markets on Edge as Input Costs Could Surge

The immediate financial market reaction has been observed in the shares of major fertilizer producers and agricultural commodity futures. Companies with global production and distribution networks, such as Nutrien Ltd. ($NTR) and The Mosaic Company ($MOS), often see volatility in such geopolitical climates. While they have diversified shipping options, any broad-based increase in freight and risk premiums affects the delivered cost of their products worldwide.

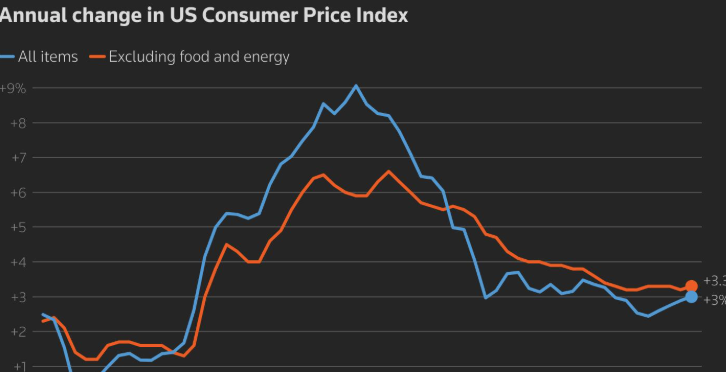

Fertilizer prices are a primary driver of farm-level production costs. The World Bank’s fertilizer price index, while down from the peaks of 2022, remains historically elevated and sensitive to supply shocks. A sustained disruption could reverse recent moderating trends. Analysts note that key growing regions in South America and Asia are entering or are in critical fertilizer application periods, making timely delivery paramount for crop yields.

Broader Implications for Global Food Inflation

The link between fertilizer costs and food prices is well-established, operating with a lag of several months. Higher input costs for farmers typically translate into higher prices for staple crops like corn, wheat, and soybeans. The UN Food and Agriculture Organization (FAO) Food Price Index has shown tentative signs of stabilization, but a new spike in fertilizer costs threatens this fragile balance.

Global food security remains a pressing concern, with inventories for several major grains still below long-term averages. A supply-driven price shock in fertilizers could pressure these inventories further by potentially reducing application rates and subsequent yields. Central banks worldwide, still grappling with inflation, monitor food price trends closely as they influence core inflation expectations and consumer sentiment.

Market Analysis and Risk Assessment

From a market perspective, the situation introduces a fresh layer of geopolitical risk premium into soft commodity futures and the equities of the agricultural sector. Traders are likely to monitor shipping data from the Gulf region and statements from major fertilizer distributors for signs of actual volume disruption versus perceived risk. The duration and scale of any shipping interference will be the key determinant of the price impact.

It is crucial to note that as of now, the market is reacting to a risk scenario. Widespread, confirmed disruptions to fertilizer shipments have not yet been reported. The situation remains fluid, and diplomatic developments could rapidly alter the risk calculus. However, the mere threat is sufficient to tighten near-term market sentiment and support prices for fertilizer products and the crops that depend on them.

Summary and Forward Outlook

Geopolitical tensions around the Strait of Hormuz have placed the global fertilizer supply chain under a spotlight, raising the specter of renewed cost pressures for farmers. While direct shipments are not yet halted, the risk premium is rising, impacting related financial markets. The situation underscores the fragility of interconnected global food systems.

The forward-looking takeaway hinges on the duration of the regional tensions. A swift de-escalation would likely see risk premiums recede. However, a protracted period of uncertainty could trigger tangible fertilizer shortages, higher agricultural production costs, and ultimately contribute to stickier food inflation in the latter half of the year, complicating monetary policy decisions globally.

Comments are closed.